.png)

There are moments in a founder's life where months of work compress into a single hour. A board meeting where the numbers don't tell the story you wanted. A Series B pitch where one wrong answer can stall the deal. An all-hands where you tell your team the product you've all been building together is fundamentally changing direction. Most advice treats these as separate problems: different playbooks, different anxieties, different prep checklists. That separation is the mistake. Board meetings, fundraising rounds, and pivots are variations of the same underlying problem: performing under asymmetric stakes, controlling narrative when the outcome is uncertain, and managing your own internal state while simultaneously managing everyone else's perception of you. The skills required don't change much. The context does. This guide addresses all three (the tactical and the psychological), including the 48-72 hour preparation window that most founders never think about, and the debrief practice that turns each high-stakes experience into preparation for the next one.

- Board meetings, fundraising rounds, and pivots all require the same core skills: narrative control under pressure, emotional regulation, and stakeholder trust maintenance.

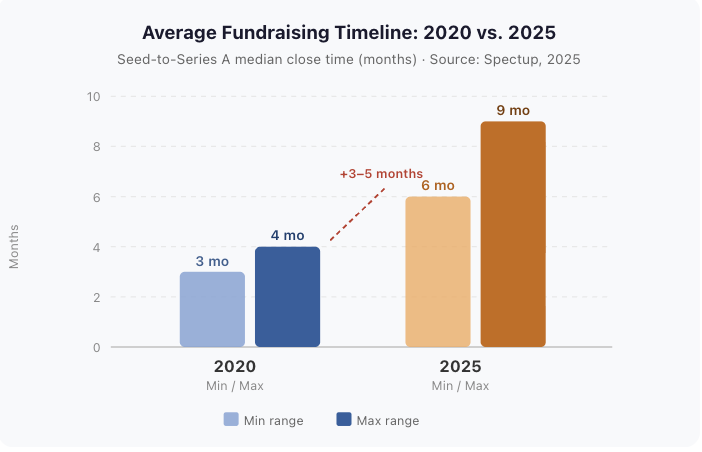

- In 2025, fundraising takes 6-9 months on average, up from 3-4 months in prior cycles, meaning founders must prepare for sustained performance across 20-30 conversations, not a single pitch (Spectup, 2025).

- Most founders over-prepare the artifact (the deck, the memo) and under-prepare the conversation: the unexpected question, the resistant board member, the hostile Q&A.

- For pivots, the announcement is harder than the decision. Almost nobody prepares for it.

- The 48-72 hours before any high-stakes event are the most overlooked performance lever in a founder's toolkit.

What Board Meetings, Fundraising, and Pivots Actually Have in Common

In 2024, Balderton Capital surveyed hundreds of founders and found that 89% describe the startup ecosystem as a high-pressure environment; 64% say sustained high pressure actively damages their business performance. That gap between pressure felt and performance delivered doesn't close by working harder. It closes through preparation.

These three events look logistically different. But they share a structural pattern that most startup advice ignores: each one is a high-stakes performance moment, not just an operational task.

The asymmetry is real. A 90-minute board meeting can reshape your company's trajectory for the next year. A 45-minute pitch can determine whether your runway extends two years or six. A 30-minute all-hands can hold your team together through a difficult transition or fracture it. The outcome is disproportionate to the time invested, and that asymmetry creates a specific kind of pressure that punishes underprepared founders.

What makes preparation hard isn't the artifacts. Most founders know how to build a board deck, draft an investor update, or write a company announcement. What trips them is the dynamic: the unexpected question, the resistant board member, the team member who challenges them in front of everyone, the investor who goes quiet and gives nothing to read.

The skills that handle those moments (holding composure, reframing a difficult question, acknowledging bad news without losing the room) are transferable across all three contexts. Founders who develop these skills in one high-stakes context carry them into the next. That's the compounding value of treating high-stakes preparation as a unified skill, not three separate checklists.

Read: Founder performance under pressure

How to Prepare for a Board Meeting — Especially When the Numbers Are Hard

According to Kruze Consulting's research on startup boards, most early-stage founders spend 8 to 12 hours preparing for each board session. Almost all of that time goes to the deck. Very little goes to the conversation itself.

Board meetings aren't primarily about reporting. They're about trust maintenance. The preparation that actually matters isn't deck polish; it's how you frame reality before anyone walks into the room.

Most of the work of a good board meeting happens before it starts. Materials should go out 5-7 days in advance, not as courtesy but as strategy. A board that's reading the deck for the first time during your presentation is processing information rather than engaging with it. You want them thinking about the future, not catching up on the past.

More importantly: schedule pre-meeting one-on-ones with board members before any meeting where the news is complicated. Call them individually. Walk through the key issues. Ask what's on their mind. This isn't leaking your agenda; it's temperature gathering. You surface objections privately, address them before anyone's in the room, and significantly reduce the chance of being blindsided by a concern that's been building for weeks.

The time structure of the meeting itself matters. The most effective early-stage board meetings follow a roughly 70/30 split: 70% on forward-looking discussion, 30% on status reporting. Most founders do the opposite, spending the first two-thirds walking through metrics that could have been read asynchronously, then leaving fifteen minutes for the strategic conversation that actually needed an hour.

The principle holds consistently: good board meetings happen before the meeting. The agenda, the pre-reads, the individual conversations determine what kind of discussion is possible in the room.

When the Numbers Are Hard: How to Structure the Narrative

When your company has missed targets (and at some point, every company does), the sequence of how you present that information matters more than the information itself.

Don't lead with the number. Lead with the honest explanation.

A narrative sequence that holds up under scrutiny: Problem → Root cause analysis → What you've already done → Forward plan → What you need from the board. This structure positions you as someone who has been working the problem, not someone announcing a problem and waiting for instructions. The board's instinctive question when they hear bad news is does this person have the situation in hand? This sequence answers that before it's asked.

The credibility cost of minimizing or delaying bad news isn't theoretical. Boards expect setbacks; they've seen hundreds of them. What they don't forgive is being managed out of the real story. A founder who soft-pedals difficult news in an investor update buys a few weeks of reduced anxiety and pays for it with compounding trust erosion. Every subsequent communication gets filtered through a quiet question: is this person telling me the real story?

Noah Shanok, who founded Stitcher (acquired by SiriusXM for $325M) and now coaches venture-backed founders, describes defaulting to optimism in investor communications as one of the most expensive patterns he's seen, and run himself. "The gap between the story you're telling and the operational reality you're living compounds," he notes. "Every overly optimistic update makes the next difficult conversation harder, because you've borrowed credibility from a future version of yourself who has to walk it back." The cost didn't arrive in one moment. It accumulated across months of small narrative inflations that slowly widened the distance between what he was reporting and what investors were observing.

A practical exercise for the evening before a difficult board meeting: run a pre-mortem on the conversation itself. Write down every question you don't want to get. For each one, write the honest answer. You'll find that most of the questions you're dreading have better answers than you expected; the ones that don't are exactly the ones you needed to prepare for, not avoid.

Honest framing, delivered early and with a clear forward plan, lands better than founders expect. Most of the fear around board transparency comes from imagining worst-case reactions, not from experience of what actually happens when you tell the truth clearly and with a plan already in motion.

What Investors Are Actually Watching Beyond the Deck

According to DocSend's pitch deck analysis, the average venture capitalist spends 2 minutes and 23 seconds reviewing a pitch deck before a meeting. That figure isn't an argument for shorter decks; it's a reminder that the deck isn't where the real evaluation happens.

Sophisticated investors make funding decisions partly on the materials and mostly on the person. What they're evaluating in the room is different from what founders typically prepare for.

They're watching how you handle uncertainty. Can you say "I don't know" without losing authority? Can you hold your position when challenged without becoming defensive? Can you receive a hard question and respond with curiosity rather than an explanation designed to make the question disappear? These are the tells. A founder who over-explains under pressure signals low confidence in the underlying business. A founder who responds with genuine engagement ("that's worth digging into; here's how I've been thinking about it") signals something different entirely.

The communication research is applicable here with appropriate framing. Mehrabian's work at UCLA established that in emotionally loaded conversations, how something is said (tone, pacing, physical presence) conveys significantly more than the words themselves. The practical implication isn't to rehearse your body language. Coached nonverbal behavior reads as performance, and experienced investors recognize it. The implication is that your internal state, which shapes your tone and presence, matters more than your slide transitions.

Deliberate pacing deserves specific attention. Founders who speak too fast under pressure are operating at cognitive capacity, having run out of bandwidth and compensating with speed. A willingness to pause before responding, to let a brief silence sit in the room, reads as cognitive reserve. It reads as someone who isn't rattled.

One skill worth explicit preparation: handling a question you can't answer. The answer is simple. "I don't have that number with me. I'll get it to you by Thursday." That's it. Don't fabricate. Don't deflect into adjacent territory. Don't minimize the question. Acknowledging the gap and committing to a specific follow-up is more credible than any answer you'd improvise on the spot.

On rehearsal: quality beats quantity. Founders who over-rehearse pitch presentations until they can deliver from muscle memory often lose the conversational quality that investors actually respond to. A better investment is pressure-testing the Q&A, having a co-founder, advisor, or coach ask the hardest questions they can generate, repeatedly, until you stop flinching at the uncomfortable ones.

How Founders Should Actually Prepare for Fundraising

In 2025, fundraising takes 6-9 months on average, nearly double the 3-4 month duration typical before 2022, according to Spectup's VC expectations research. That timeline shift changes everything about how founders should approach preparation, pacing, and emotional management across a raise.

The most important implication: fundraising isn't a performance you deliver once. It's a sustained campaign requiring you to show up at your best across 20-30 investor conversations, distributed over months, while simultaneously running your company. Preparation that only optimizes for a single excellent pitch is inadequate preparation.

Treat the fundraising pipeline the way you'd treat a sales pipeline. Stage every investor, track their position in the process, manage follow-up cadence deliberately, and pay attention to pipeline velocity, not just individual meeting quality. A pipeline that stalls across multiple investors simultaneously usually signals a narrative problem, not a quality problem.

Your pitch will evolve over the course of a raise. The first several conversations teach you which parts of your story resonate and which generate friction. That feedback should inform how you present, but the core thesis must stay coherent across the process. Investors talk to each other. Inconsistency in your narrative reads as uncertainty in your conviction.

The storytelling-versus-honesty tension is real. Optimistic framing is expected in investor pitches. Pattern-matching investors, though, will detect gaps between the story you're telling and the numbers you're showing. The version of your company that exists in the pitch needs to be close enough to the version in the data room that diligence confirms your narrative rather than complicating it.

The Rejection Endurance Problem

Each fundraising rejection hits the same neural pathway as personal rejection, because for many founders, the company is personal. The identity fusion between founder and company means that a VC passing on the deal can register as a verdict on you as a person. That's worth naming explicitly, because it affects both decision-making and stamina across a long raise.

Rejection in fundraising is structurally normal. Most founders need 20-30 investor conversations to reach a term sheet. The volume of "no" is a feature of the process, not a signal about company quality.

One practical technique: convert emotional accumulation into analytical data. Tracking rejections systematically (who passed, what the stated reason was, whether the feedback contained signal worth incorporating) creates analytical distance from the emotional weight. The record becomes data rather than wound.

Before raising Stitcher's first institutional round, Noah Shanok was rejected by approximately 90 venture capital firms. He kept a spreadsheet. Every rejection was logged: firm, partner, stated reason, date. The spreadsheet did something important: it converted a mounting emotional experience into a manageable analytical one. It also produced data. When Benchmark and NEA eventually invested, Noah had a clearer picture of which parts of his pitch had consistently worked and which had required iteration. The discipline of tracking was partly emotional hygiene and partly intellectual rigor, a way of treating the fundraising process as something to learn from rather than simply survive.

Not all rejection contains useful signal. A pass from a fund that doesn't invest in your stage, sector, or geography tells you nothing about your company. The skill is distinguishing the feedback that warrants updating your narrative from the feedback that reflects investor fit, then moving through the latter quickly.

Pivot Preparation: The Decision Is the Easy Part

Y Combinator partners have documented pivot stories across hundreds of portfolio companies, including Brex, Slack, and Instagram, finding that significant directional changes are the norm rather than the exception among successful startups. What those pivot histories consistently omit is the announcement: the investor call, the all-hands, the conversation with team members whose work was just declared obsolete.

The decision is the easy part. The announcement is harder. And most founders aren't prepared for it.

Once you've decided to pivot, you have three separate communication problems: investors, team, and customers. Each requires a different approach, a different sequence, and a different emotional register. Most pivot guidance addresses the investor conversation briefly and skips the rest entirely.

How to Tell Your Investors About a Pivot

Don't announce a pivot in a group board meeting. Do it in pre-meeting one-on-ones or individual investor calls first, every time.

Re-pitching investors on a new thesis is structurally different from pitching cold. You're managing their existing mental model of your company while simultaneously selling them on a new direction. They've already made a bet on a specific version of your vision. You're asking them to believe that bet still makes sense, just from a different angle.

A narrative architecture that works: What you learned → Why the original thesis was incomplete, not wrong → What the new data shows → Why this pivot improves the asset they've already invested in. That last element matters. You're not telling them their investment failed; you're telling them the path to making that investment work is different from what you originally mapped together.

The credibility trap applies here with particular force. Founders who've been consistently optimistic in investor updates have less narrative runway when they need to make a significant course change. The accumulated cost of inflated storytelling is paid most visibly when you need your investors to trust a move they didn't anticipate.

How to Tell Your Team About a Pivot

The sequence for internal communication is non-negotiable: your leadership team first (privately, with the full reasoning and time to react), then the broader company. Never the reverse.

An announcement architecture that holds up: Context → Decision → Rationale → What changes and what stays the same → What you need from them. The context section is often skipped. Don't skip it. People can absorb difficult information when they understand the reasoning; they struggle when they're handed a conclusion without the path that led to it.

The identity dimension of a pivot is frequently underestimated. For team members who've been building a specific product or working toward a specific vision, a pivot isn't just a strategic update; it's a loss. The work they cared about, the expertise they built, the thing they were proud of: some of it won't carry forward. Acknowledging that explicitly, without minimizing it, changes the emotional register of the conversation.

Structure the Q&A. Plan for it rather than treating it as an afterthought. Unanswered questions in a room of uncertain people don't disappear; they circulate in Slack channels and parking lot conversations and fill with anxiety. A structured Q&A session with honest answers (including "I don't know yet, and here's when I will") is almost always more stabilizing than a polished monologue with no room for response.

A pattern Noah Shanok encounters consistently when coaching founders through pivots: the delay in internal communication isn't usually about logistics. It's about fear. Founders hold off telling the team because they're afraid of eroding confidence: in themselves, in the company, in the direction they've chosen. But the delay creates exactly the confidence problem they're trying to avoid. The team can tell something is happening. Silence in the face of visible uncertainty is never neutral; it just means the story gets filled in without you.

The 48-72 Hour Preparation Window That Most Founders Ignore

In 2024, Balderton Capital found that 64% of founders report sustained high pressure negatively impacts their business performance. What's less often discussed is that performance tends to be most vulnerable in the days immediately before a major event, when the pressure is highest and preparation habits are worst.

The most overlooked element of high-stakes preparation isn't the deck, the financial model, or the narrative framework. It's the 48-72 hours before the meeting, and the cognitive state you arrive in.

Performance isn't fixed. It fluctuates with sleep quality, physical recovery, accumulated stress load, and anxiety that hasn't been processed. The preparation paradox is that founders often do their worst preparation work in the 48 hours before a major event, precisely because that's when they're most stressed. They stay up late revising slides, run on caffeine, skip exercise, and walk into the most important meeting of the quarter already depleted.

Sleep is a performance input, not a lifestyle choice. Sleep debt accumulated over several nights isn't recoverable in a single early bedtime, but two nights of quality sleep (consistent wake time, no screens in the final hour, no alcohol, phone outside the bedroom) makes a measurable difference in working memory, verbal fluency, and emotional regulation. These are exactly the capacities that determine how you respond to unexpected questions, hold your composure when the room is difficult, and think clearly when challenged.

Mental rehearsal is different from deck rehearsal. The night before a major meeting, close the laptop. The deck is ready or it isn't. What's worth doing instead: run the conversation in your head. Imagine the hardest question you could be asked. Imagine the moment you stumble. Imagine the board member who challenges your numbers, or the investor who sits quietly for thirty minutes and gives you nothing to read. Rehearse the recovery, not the performance. What do you say when you don't know the answer? How do you re-anchor after a difficult exchange? That rehearsal does more than another pass through your slides.

The pre-mortem, applied the evening before. Twenty minutes. Write down every way the meeting could go wrong. For each scenario, write one sentence on how you'd handle it. This exercise does two things: it converts ambient, floating anxiety into specific scenarios (which are manageable), and it gives your brain permission to stop running background threat-assessment loops during the meeting itself. You've already processed the threats. You can be present.

On physical state: heavy exercise 24-48 hours before a major meeting tends to improve subsequent cognitive performance. The morning of the meeting, light movement (a walk, not a workout) and moderate caffeine are better than the alternative most founders default to: no sleep, maximum caffeine, adrenaline substituting for preparation.

During Stitcher's fundraising process, Noah Shanok was sleeping around four to five hours a night and relying heavily on caffeine to sustain the pace. He performed poorly in one consequential investor-related meeting, struggling with recall and cognitive processing in a room where neither was optional. Later in the process, before the meeting with Benchmark that led to the investment, Noah had deliberately prioritized sleep in the preceding days. He arrived rested, focused, and able to think clearly under pressure. He credits that shift (not a sharper deck, not a better pitch, but a better-rested brain) as a material factor in how that meeting went. Sleep was the performance leverage he'd been leaving on the table throughout the raise.

Why the Debrief Is the Most Underused Preparation Tool

Research by psychologist K. Anders Ericsson on deliberate practice found that structured feedback loops after performance events accelerate expertise development more reliably than accumulated experience alone. Founders face no shortage of high-stakes experience. The ones who improve fastest are the ones who debrief it.

Every high-stakes event produces information that can improve the next one. Most founders don't capture it.

The useful debrief window is 24-48 hours after the event, long enough to have some distance but short enough that the details are still fresh. The format doesn't need to be elaborate. Four questions are enough:

- What worked that I should repeat?

- What failed that I need to fix?

- What question caught me completely off-guard?

- What do I wish I'd said differently?

These four questions, answered honestly after every significant board meeting, investor pitch, and pivot announcement, generate pattern recognition over time. You start to see which questions you're consistently underprepared for. You notice the narrative framing that reliably lands with a particular board member and the framing that reliably generates resistance. You recognize the pre-meeting dynamic that tends to predict a difficult room, and you start managing it earlier.

Close the loop with board members after every meeting. A brief email within 24 hours (action items, key decisions made, commitments from the meeting, next steps) is a trust-compounding gesture that most founders skip entirely. It signals organization, follow-through, and that you took the conversation seriously enough to document it. Board members notice who sends these and who doesn't.

The compounding principle: each high-stakes event builds capacity for the next one, but only if you capture the learning. Founders who debrief consistently improve systematically at exactly the moments that matter most. Founders who don't have to re-learn the same lessons under the same pressure, each time.

Read: Self-awareness and leadership development

Frequently Asked Questions

How early should a founder send board materials before a meeting?

Materials should go out 5-7 days in advance, not as an administrative courtesy but as a strategic choice. A board reading the deck for the first time in the meeting is processing information, not engaging with it. Earlier distribution lets board members come in with questions rather than reactions, which produces materially better conversation and allows you to spend meeting time on what actually matters: forward-looking decisions.

What should founders do when they've missed targets before a board meeting?

Lead with the honest explanation, not the number. A sequence that holds up: Problem → Root cause analysis → What you've already done → Forward plan → What you need from the board. Do pre-meeting one-on-ones with each board member before walking into the room. Boards expect setbacks; what they don't forgive is being managed out of the real story. The credibility cost of minimizing bad news compounds over time and is paid most visibly when you need their trust most.

How do founders manage investor rejection during fundraising without losing momentum?

Track rejections analytically (who passed, stated reason, whether the feedback contained real signal) rather than absorbing them as personal verdicts. Most rejections reflect investor fit or timing, not company quality. Treating the record as data rather than wound creates analytical distance from the emotional weight. The volume of rejection is structurally normal: most founders need 20-30 investor conversations per term sheet, meaning the process is designed to produce many nos before a yes.

When is a startup pivot too late?

Most founders know the answer earlier than they act on it. The analytical signals are well-documented: CAC exceeding LTV over multiple quarters, retention declining despite dedicated product effort, team disengagement from the roadmap. But the delay between knowing and acting is almost always psychological, not analytical. The fear of what a pivot implies about the original vision, the reluctance to disappoint the team, the hope that one more quarter of data might change the picture: these are the actual barriers to timely pivots, and they're worth naming honestly.

How do you tell your team about a pivot without losing them?

Sequence matters: inform your leadership team privately first, with full reasoning and time to react, before any broader announcement. The architecture that holds up: context (why we're here) → decision → rationale → what changes, what stays the same → what you need from them. Acknowledge explicitly that for some people, this is a loss. Structure a dedicated Q&A rather than leaving questions to fester. Honest answers, including "I don't know yet," are more stabilizing than a polished announcement with no room for response.

Read: Startup CEO Coach Blogs, by Noah Shanok

Sources

- Balderton Capital, Start-up Founders Under Greater Pressure Than Ever as Research Reveals Diminishing Returns from Ever-Increasing Hours, retrieved 2026-05-14, https://www.balderton.com/news/start-up-founders-under-greater-pressure-than-ever-as-research-reveals-diminishing-returns-from-ever-increasing-hours/

- Spectup, VC Expectations in 2025: What Founders Keep Missing in Fundraising, retrieved 2026-05-14, https://www.spectup.com/resource-hub/vc-expectations-in-2025-what-founders-keep-missing-in-fundraising

- DocSend (Dropbox), Pitch Deck Interest: How Much Time Do Investors Really Spend?, retrieved 2026-05-14, https://docsend.com/blog/how-long-vc-spends-on-pitch-deck/

- Kruze Consulting, Startup Board Meetings: The Complete Guide, retrieved 2026-05-14, https://kruzeconsulting.com/blog/startup-board-meetings/

- K. A. Ericsson, R. T. Krampe, and C. Tesch-Römer, The Role of Deliberate Practice in the Acquisition of Expert Performance, Psychological Review, Vol. 100, No. 3, 1993

- A. Mehrabian and S. R. Ferris, Inference of Attitudes from Nonverbal Communication in Two Channels, Journal of Consulting Psychology, Vol. 31, No. 3, 1967