.png)

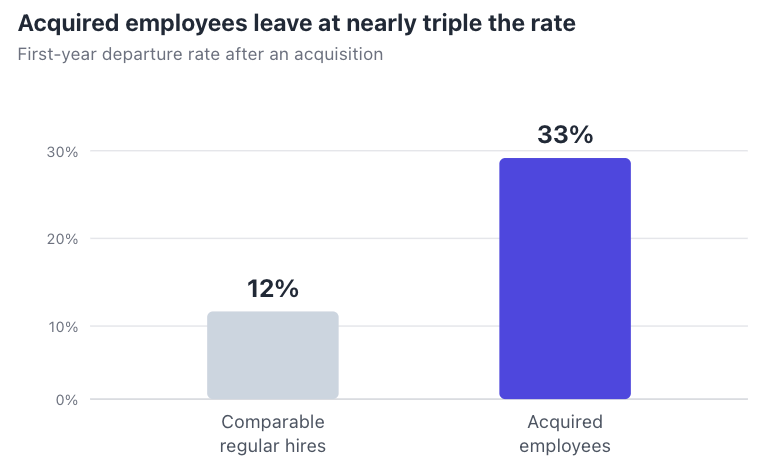

The deal is the part everyone pictures: the term sheet, the wire, the announcement. But by the time a letter of intent lands on a founder's desk, the decisions that shaped the outcome were mostly made months earlier. An exit doesn't just change a founder's net worth. It changes the job, quietly, from building the company to representing it, while the founder is still the only person who can't tell the team what's happening. And the strain shows up in the data long after the deal closes: acquired employees leave at roughly 33% in their first year, versus 12% for comparable regular hires (MIT Sloan, 2023). For the founder at the center of it, the work of leading through an exit starts well before the price is set, and rarely ends when the deal does.

Key Takeaways

- Acquired employees leave at about 33% in year one, versus 12% for comparable regular hires, so retaining a team through a deal is harder than it looks (MIT Sloan, 2023).

- The highest-leverage exit decisions happen before the LOI, when the founder still has clarity and leverage to set terms, timing, and their own definition of success.

- During a live deal, the founder works two full-time jobs at once: running the transaction and running the company that's being sold.

- The hardest leadership problem is the communication tightrope, leading a team you're legally unable to tell.

- A successful exit can still feel hollow, because the founder's identity was fused to the thing they just handed over.

What changes when an exit goes on the table?

When an exit becomes real, the founder's job changes before the company does. The role quietly splits in three: the founder is now the seller, still the leader, and the person whose identity is bound up in the thing being sold. Most coaching content addresses either the deal mechanics or the post-exit comedown. The live transaction window, where a founder is most alone, gets skipped.

That gap matters because the transaction is where judgment, communication, and self-honesty get tested hardest, all at once, and usually under a compressed timeline. The founder is negotiating with a counterparty they may have to work for afterward, reassuring a team they can't read in, and quietly deciding what they actually want from the outcome. None of that is in the data room.

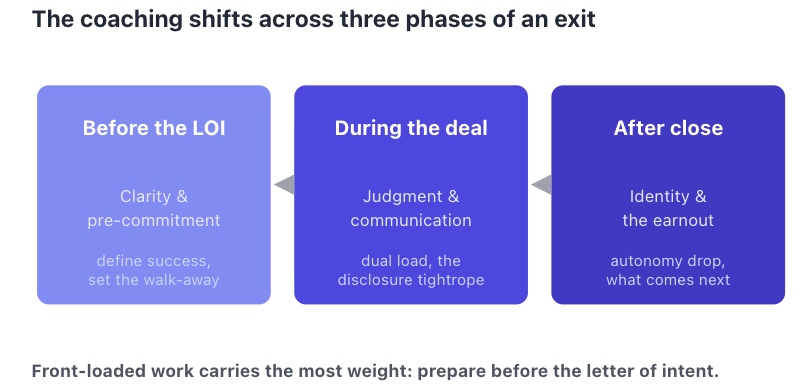

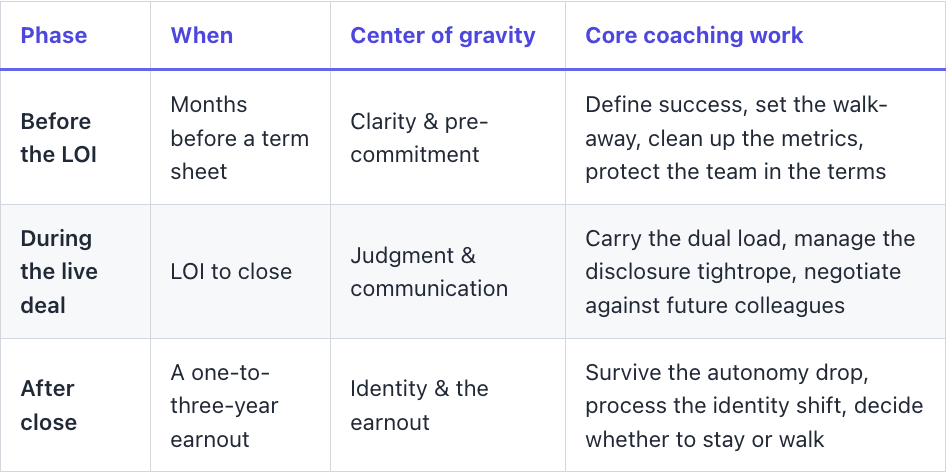

This piece maps how the coaching work shifts across three phases: the months before the letter of intent, the live deal itself, and the period after close, when the earnout and the identity questions arrive together. The thread running through all three is that the most consequential work is front-loaded. The founder who does it early suffers least later.

Why do the most important exit decisions happen before the LOI?

By the time a letter of intent arrives, most of a founder's leverage is already spent. The decisions that determine the outcome, whether to run a process or take an inbound, who sits in the room, how clean the metrics are, and what the founder actually wants, get made in the quiet months before any number is on the table.

That last one is the decisive piece, and the easiest to skip. A founder who hasn't defined success in advance lets the number define it for them. Is the priority liquidity, the mission's survival inside a larger company, or the team's outcome? Those goals pull in different directions, and a term sheet is a bad place to discover you never chose. Coaching here isn't negotiation tactics. It's clarity and pre-commitment: naming your walk-away and your non-negotiables while you can still think straight.

The pattern repeats one founders know from fundraising. The work that makes a high-stakes moment go well happens before the room, not in it. The same discipline that prepares a founder for a pivotal board meeting or a raise applies to an exit, and it's worth studying directly in how founders prepare for high-stakes board and investor moments.

Knowing what you actually want from the exit

Liquidity, legacy, freedom, the team's future: a founder can't optimize for all of them, and an acquirer's offer will quietly favor whichever one the founder hasn't defended. Naming the real priority before the process starts is what keeps the deal from choosing on your behalf. It's also the single most useful thing to work through with someone who has no stake in the answer.

How does a founder's role change during a live deal?

During a live deal, the founder takes on a second full-time job without putting down the first. Diligence requests, banker and lawyer calls, and board management stack on top of running the company, and the timeline is rarely generous. The result is decision fatigue arriving exactly when the decisions are largest.

That cognitive load isn't a soft concern. Judgment runs on a body, and it degrades quietly under sleep loss and sustained stress, the standard conditions of a deal sprint. Founders who have watched their own thinking get slower under pressure tend to take this seriously; the link between rest and decision quality is covered in how much sleep a founder actually needs and how to make faster decisions as a CEO.

There's also a relationship trap hiding inside the negotiation. The founder is bargaining against people who may soon be their employer or their colleagues. Push too hard and you poison the working relationship you'll inherit; push too softly and you leave the team's interests on the table. Holding both at once, advocate and future teammate, is a balancing act few founders have practiced, and it's where an outside sounding board earns its keep.

The communication tightrope: leading a team you can't tell

The hardest leadership problem in a live deal is that the founder must keep a team steady while being legally unable to explain why things feel different. The founder carries information that would change everyone's decisions and can't share it. That asymmetry, not the deal terms, is what keeps founders up at night.

It's also where over-reassurance does real damage. Vague optimism to buy calm works the same way it does with investors: the gap between the story and the reality compounds, and credibility erodes when the truth finally arrives. The discipline of choosing candor over comfortable optimism, explored in how to balance transparency against optimism with investors, is exactly the muscle a founder needs when a deal is in motion and the team senses something unspoken.

The stakes are concrete. Research from MIT Sloan's Daniel Kim, drawing on matched U.S. Census data across roughly 4,000 acquisitions, found that acquired employees leave at about 33% in their first year, compared with 12% for comparable regular hires, with year-one retention of 66% versus 88% (MIT Sloan, 2023). A founder who protects the team's interests in the deal terms, then plans the disclosure carefully, is fighting directly against that attrition.

So the disclosure question, when and how to tell the team, isn't a comms detail. It's a retention decision. Sequencing the announcement, getting ahead of the retention conversation, and being honest about what you can and can't say are how a founder keeps the people who make the company worth buying.

Why do successful exits still feel hollow? The identity problem

Founders routinely report feeling flat, lost, or grief-stricken after an exit that went well, not because the deal was bad, but because their identity was fused to the company they just handed over. The startup was the daily mission, the social world, the source of status and urgency. All of it disappears at once.

This is a predictable transition, not a personal failing, and naming it in advance softens the landing. Academic work on entrepreneurial exit points the same direction: leaving a venture is associated with measurable declines in founder well-being, with strong personal and online networks buffering the effect (ECIS Proceedings, 2026). The number isn't the point; the direction is. Exit, even a triumphant one, tends to cost something psychological.

Here's where coaching during a deal differs from therapy after one. Most content treats the identity question as post-close grief to process in hindsight. The more useful move is to surface it forward-looking, while the deal is live, so the founder can prepare for the shift before it lands rather than discover it in the silence afterward. The question worth sitting with before the wire clears is simple and uncomfortable: who are you when the company isn't yours anymore?

What happens after the deal closes: earnouts and golden handcuffs

For many founders, the exit isn't an exit. It's a new job inside someone else's company. Earnout and retention structures commonly keep a founder employed at the acquirer for one to three years, chasing milestones with far less control than they had as CEO. The clean break most people imagine is the exception.

The psychological adjustment is steep: from founder-CEO to a manager inside an unfamiliar org, with diminished autonomy and politics you didn't design. Motivation gets complicated when your remaining equity is tied to targets you no longer fully control, and resentment is an occupational hazard. There's evidence founders are kept on more than outsiders assume: research in the Journal of Management Studies finds that founder-CEOs of acquired firms are retained at higher rates than professional CEOs, an effect strongest in technology-driven deals (Journal of Management Studies, 2022). Staying is often the expectation, not the exception.

From founder to employee: the autonomy adjustment

The practical work here is redefining the role on your own terms, picking which battles are worth fighting inside a bigger system, and protecting your own mental health through a stretch that can feel like a long goodbye. It also means an honest decision: serve out the earnout, or walk and leave money on the table? That trade-off, autonomy and well-being against the remaining payout, deserves a clear-eyed conversation, not a default. The same strain that drives founder burnout in the build phase shows up here in a different costume; how startup CEOs avoid burnout applies directly to the retention period.

What does a coach actually do during an acquisition?

An executive coach during M&A isn't a banker or a lawyer. The job is to keep the founder's judgment, communication, and self-honesty intact while every other party in the deal optimizes for their own outcome. It's the one relationship in the process with no competing interest.

That neutrality is the whole value. The founder can't fully confide in the team, shouldn't lean on the board, and certainly can't think out loud with the acquirer. A coach is the unconflicted room where a founder can pressure-test a decision under fatigue, rehearse a hard conversation, and say the quiet part before saying it where it counts. Noah Shanok, founder and former CEO of Stitcher, the podcast platform later acquired by SiriusXM for $325 million, built his coaching practice on this operator's vantage point: someone who has run a company day to day tends to recognize the patterns a founder is living through.

One pattern matters more than any other in a deal. Founders usually know the difficult truth, take the offer, walk away, or finally tell the team, well before they act on it, and they delay out of fear, guilt, or fading confidence. The same dynamic shows up across founder decisions and is unpacked in why CEOs avoid the decisions they already know they need to make. A coach's job in an exit isn't to supply the answer. It's to shorten the distance between knowing and acting, when the clock is running and the stakes are personal. Startup CEO Coach works with venture-backed founders on exactly these moments.

A practical framework: coaching across the three phases of an exit

The coaching work maps cleanly onto three phases, each with a different center of gravity. Before the LOI, the work is clarity and pre-commitment. During the live deal, it's judgment and communication under load. After close, it's identity and the earnout. The highest-leverage work sits at the front; the founder who prepares before the LOI carries the least weight later.

The same three phases, read as a reference table:

A short pre-deal checklist for founders

Before a letter of intent shows up, a founder can pressure-test their own readiness with a handful of questions:

- What do I actually want from this, in priority order, liquidity, legacy, the team, or freedom?

- What's my real walk-away, the terms I won't cross no matter the number?

- Who needs to be in the room for this process, and who doesn't?

- Are my team's interests protected in the structure I'm imagining?

- Who is my confidential thinking partner through this, someone with no stake in the answer?

- Have I named the identity shift that's coming, before it arrives?

A founder who can answer those calmly is in a very different position than one improvising after the LOI lands.

When should a founder start coaching for an exit?

The best time is before the letter of intent, when leverage and clarity are still high, not after the deal is moving and choices have narrowed. Most founders bring in support too late, once the transaction is already pulling them in two directions. By then the early, high-leverage decisions, what you want, how clean the story is, what you'll defend, are largely behind you.

What founders tend to value, judging by their feedback on working with Noah Shanok, is a coach who has actually operated, can tell the difference between a real risk and a nervous one, and helps them act on what they already sense rather than circling it. An exit compresses every founder pressure, decision-making, communication, identity, into a short and consequential window. Going through it with one genuinely neutral person in your corner is not a luxury at that stage. It's infrastructure.

Frequently Asked Questions

Do founders usually stay at the company after it's acquired?

Often, yes. Earnout and retention agreements commonly keep founders employed at the acquirer for one to three years. Turnover is still high: acquired employees leave at about 33% in year one versus 12% for comparable regular hires (MIT Sloan, 2023), and founder-CEOs are typically retained at higher rates than outside CEOs.

Why do founders feel depressed after a successful exit?

Because identity fuses with the company, and an exit removes the mission, status, daily structure, and social world all at once. Research on entrepreneurial exit associates it with measurable declines in founder well-being, buffered by strong networks (ECIS Proceedings, 2026). It's a normative transition, not a failure, and naming it early helps.

What does an executive coach do during M&A?

A coach is the founder's one unconflicted thinking partner while bankers, lawyers, the board, and the acquirer all pursue their own interests. The work is protecting judgment under fatigue, preparing high-stakes conversations, managing the team-communication tightrope, and shortening the gap between the decision a founder already senses and acting on it.

When should a founder hire a coach before selling the company?

Before the letter of intent, when clarity and leverage are highest. The most consequential exit decisions, defining what you want, setting your walk-away, cleaning up the metrics, and protecting the team, happen in the quiet months before a number is on the table, not during the negotiation itself.

How do you keep a team motivated during an acquisition?

Protect their interests in the deal terms, then handle disclosure deliberately rather than reassuring vaguely. With acquired-employee attrition near 33% in the first year (MIT Sloan, 2023), sequencing the announcement, getting ahead of retention conversations, and being honest about what you can and can't say are what hold the team together.

Is Noah Shanok experienced with founders navigating an exit?

Noah Shanok is founder and former CEO of Stitcher, the podcast platform acquired by SiriusXM for $325 million, and a startup CEO coach who works with venture-backed founders from Seed to Series C, including those weighing or going through acquisitions. His coaching draws on an operator's view of founder decision-making, communication, and pressure.

Sources

- MIT Sloan (Daniel Kim), "Your acquired hires are leaving. Here's why" (based on Predictable Exodus: Startup Acquisitions and Employee Departures; matched U.S. Census data across ~4,000 acquisitions and ~350,000 employees, 1990–2011: acquired employees leave at ~33% in year one vs. 12% for comparable regular hires; year-one retention 66% vs. 88%), retrieved 2026-06-16, https://mitsloan.mit.edu/ideas-made-to-matter/your-acquired-hires-are-leaving-heres-why

- Aghasi, Colombo & Rossi-Lamastra, "Acquisitions of Small High-Tech Firms and the Retention of Target Founder-CEOs," Journal of Management Studies 59(4): 958–997 (founder-CEOs of acquired firms retained at higher rates than professional CEOs; effect strongest in technology-driven deals), 2022, retrieved 2026-06-16, https://ideas.repec.org/a/bla/jomstd/v59y2022i4p958-997.html

- "Who Am I Without My Startup? Entrepreneurial Exit, Mental Health, and the Role of Online Networks," ECIS 2026 Proceedings (entrepreneurial exit associated with measurable declines in founder well-being; strong online networks buffer the effect; directional finding, used qualitatively), 2026, retrieved 2026-06-16, https://aisel.aisnet.org/ecis2026/gen_track/gen_track/22/

- Harvard Business Review, "The Challenge of Retaining Startup Talent After an Acquisition" (contextual reference on post-acquisition retention dynamics), February 2024, retrieved 2026-06-16, https://hbr.org/2024/02/the-challenge-of-retaining-startup-talent-after-an-acquisition