.png)

Most first-time CEOs have hired people, sold to skeptics, shipped products, and closed a round before they ever run a board. Board management is the one leadership skill that arrives fully formed, with no low-stakes version to practice on first. And it lands in the highest-stakes, lowest-frequency forum a founder has: a room of people who can, if it comes to it, replace them.

That is why it goes wrong so often. The instinct is to treat the board as a quarterly exam to pass. The skill is to treat it as a relationship you run continuously, between the meetings as much as in them. The CEOs who do it well manage three moving parts: how they share information, how they build alignment before a vote, and how they disagree without spending down their credibility. This piece works through all three.

Why is managing the board the least-practiced skill for first-time CEOs?

In a 2025 Strategic Management Journal study that tracked first-time CEOs across four venture-backed startups, Sam Garg and colleagues found that the CEO–board relationship usually settles within about two years, and that how a CEO manages it early shapes whether the board backs them or moves to replace them (Garg et al., 2025). No other CEO skill carries that much weight with so little practice behind it.

Here is the structural problem. Every other muscle a founder builds has a training-wheels version. You managed one report before you managed a team. You pitched a friend before you pitched a fund. But you never had a small, low-stakes board to learn on. The first board you run is a real one, with real power, meeting a handful of times a year.

So new CEOs default to the wrong instinct: they try to impress the board. They arrive with a polished story and a rounded-up number. The actual skill is quieter, to inform the board so completely that nobody in the room is ever surprised. Impressing is a performance. Informing is a habit, and habits are what boards learn to trust.

There is also a mindset flip hiding underneath all of this. A board is not your boss in the way a manager was your boss. It is a resource you assemble and direct, a group whose judgment, networks, and capital you are responsible for putting to work. Founders who internalize that ("I manage this room; it does not manage me") tend to lead their boards. Founders who don't tend to get led by them.

Noah Shanok, founder and former CEO of Stitcher, who managed the company's board through multiple institutional financing rounds, coaches founders that the board relationship is learned live, on the job, and that the ones who struggle most are treating each meeting as a test instead of a working session. That reframe, from exam to working relationship, is where good board management starts.

What does a startup board actually do, and how does its power shift as you raise?

A startup board hires and fires the CEO, approves the decisions that reshape the company (financings, budgets, option pools, an eventual sale), and holds a fiduciary duty to all shareholders. In a 2025 study in the Journal of Finance, economists Michael Ewens and Nadya Malenko showed that a founder's control of that board erodes in a predictable pattern with every round raised (Ewens & Malenko, 2025).

The board itself is usually three kinds of people: founders, investor directors who came with the money, and independents brought in for expertise or as neutral parties. That is the composition. What matters for managing the relationship is not how you staff the seats but how the balance of power moves once they're filled.

And it moves in a set order. Ewens and Malenko found that a typical board starts entrepreneur-controlled. Independent directors join the median board after the second financing, at which point control becomes shared and those independents hold a tie-breaking vote. At later stages, control shifts to the VCs. The independents, in other words, often end up deciding (Ewens & Malenko, 2025).

Why does this matter for the relationship rather than the org chart? Because trust is the only asset that doesn't dilute. The earlier you build a communication habit and a track record of doing what you said, the more goodwill you've banked before the math tilts toward the people who can outvote you. (If you need the mechanics of staffing the seats, seat ratios and when to add an independent, that's a formation question; this piece assumes the board already exists.)

Dynamic 1: How much should you tell your board between meetings?

More than feels necessary, and on a rhythm they can predict. McKinsey's guidance for CEOs frames the board as a strategic partner run on one rule above all: no surprises (McKinsey, Navigating the Board and CEO Relationship). In board relationships it's surprise, not bad news, that destroys trust. A board can price in a missed quarter it saw coming. It cannot forgive learning about it in the room.

That rule turns "communication" into a system rather than a mood. The backbone is a short written update on a set cadence, sent even in months with no meeting. Good updates are scannable and honest: metrics against plan, a genuine win or two, the one or two things keeping you up at night, and any specific ask. The worrying number goes in the update before it becomes a crisis, not after.

Cadence norms are worth naming, but treat them as practitioner consensus, not hard data, because there's no authoritative survey on how often startup boards actually meet. In practice, seed-stage boards tend to meet roughly monthly or every six to eight weeks; growth-stage boards move to quarterly. The written update, though, stays monthly the whole way through. The meeting frequency drops; the information flow shouldn't.

The one-sentence version: No director should hear important news for the first time in a board meeting. If they do, the problem isn't the news, it's the cadence.

This is also where a specific founder failure mode shows up. The instinct to manage optimism, to frame every setback as nearly solved, feels like leadership in the moment and reads as evasion over time. The gap between the optimistic story and the operational reality compounds with every meeting it's left open. (It's worth being deliberate about balancing transparency and optimism with investors; the cadence is where that balance is either kept or lost.)

What should go in a monthly board update?

Keep it tight and the same shape every month, so directors learn where to look:

- Metrics vs. plan: the three or four numbers that define the business, against what you said last time.

- What's working: one or two real wins, briefly.

- What's worrying you: the one or two risks you're actively watching. This is the section that builds trust.

- Decisions coming: what you'll bring to the board next, so nothing is a cold open.

- Asks: specific, named help. A board can't act on "wish us luck."

Dynamic 2: How do you pre-wire board decisions before the meeting?

You never let a board vote be the first time a director hears a proposal. Pre-wiring mirrors what McKinsey's CEO guidance calls cultivating directors one-on-one between meetings: you socialize every significant decision in private conversations before it reaches the agenda (McKinsey, 2025). The meeting then ratifies alignment you've already built instead of manufacturing it live, in front of an audience. Done right, it has almost no suspense in it. That's the goal.

Let's be precise about what pre-wiring is and isn't, because it's easy to hear it as manipulation. It isn't lobbying a faction or splitting the board. It's the opposite of a surprise: you walk each director through the reasoning privately, ask for their read, and surface objections while there's still time to address them. A private objection is a conversation. The same objection raised publicly, cold, becomes a fight nobody planned to have.

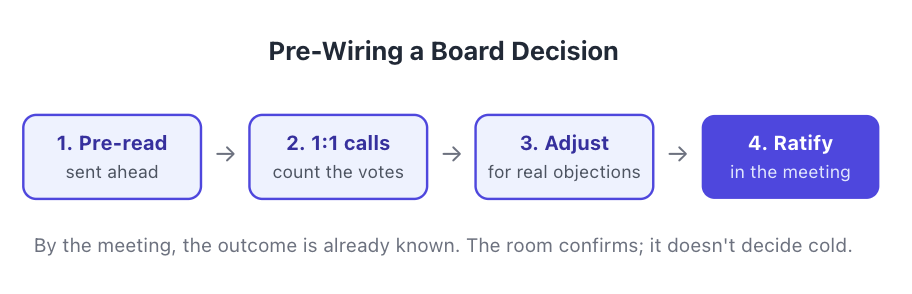

In practice, pre-wiring runs in four steps:

- Send the pre-read ahead of the meeting so every director arrives informed, not cold.

- Hold one-on-one calls: walk each director through the reasoning, ask for their read, and count the votes in advance.

- Adjust the proposal for the legitimate objections those calls surface, while there's still time.

- Ratify in the meeting, which now confirms a decision rather than deciding it live.

Why does it work? Because directors, like anyone, dislike being outvoted or blindsided in front of their peers. Give them the reasoning in private and a chance to shape it, and they walk into the meeting as co-authors rather than judges. The meeting then becomes what it should be, a working session on the two or three questions that are genuinely still open. For the mechanics of running the meeting itself, the materials, the agenda, the way you sequence bad news, it's worth studying how to prepare for high-stakes moments like board meetings separately; pre-wiring is what happens in the days before that.

Which decisions are worth pre-wiring?

Not everything. Pre-wire the decisions that change the shape of the company or touch the board's own authority:

- Financings and anything affecting the cap table or option pool.

- A pivot or a material change to strategy or burn.

- Senior hires and fires, especially at the executive level.

- Anything the board must formally approve, where a surprised "no" is expensive.

The routine and the reversible don't need this treatment. Save the effort for the calls where a cold vote could actually go wrong.

Dynamic 3: How do you handle disagreement with your board without losing the room?

You argue the substance hard and protect the relationship harder. The objective is never to win a single board fight; it's to keep enough credibility that the board still backs your judgment on the next ten decisions. A CEO who wins the argument and loses the room has made a bad trade, even when they were right.

Start by reframing disagreement itself. A board that never pushes back isn't a gift; it's a rubber stamp, and a rubber stamp is worthless exactly when you need judgment most. Dissent is a sign the board is doing its job. The question isn't how to avoid it. It's how to be on the other side of it without damage.

Think of it as a credibility bank. Every accurate forecast, every commitment delivered, every problem you flagged before you had to is a deposit. Every surprise, every rounded-up number, every "we've basically solved it" that turns out untrue is a withdrawal. When you disagree with your board, you're spending down that balance. Founders who've been quietly over-promising discover the account is empty at the worst possible moment, mid-disagreement, when they most need the benefit of the doubt.

According to the 2025 Strategic Management Journal study, CEO–board relationships tend to stabilize within about two years, and boards move to replace CEOs whose relationship has turned negative by then (Garg et al., 2025). Disagreements don't sink CEOs; a depleted credibility balance does.

So how do you disagree well? Separate the person from the position, and steelman the director's view before you counter it. Distinguish the decisions that are genuinely yours from the ones that are the board's to make. Know when to concede a small point to hold authority on a large one. And when the board is right and you're wrong, change course visibly; publicly updating on good evidence builds trust rather than costing it.

The hardest version is sustained, fundamental disagreement, the board wants to replace you, or push a sale you don't believe in. Name it honestly rather than maneuvering around it, focus on what you can actually control, and get counsel from someone with no stake in the outcome. Everyone inside that room, investors, co-founders, the board itself, has a position. Which is exactly why founders under this kind of pressure often need one relationship that doesn't.

What are the warning signs of a dysfunctional board relationship?

The earliest signals are informational, not emotional. When directors start learning key news from someone other than the CEO, when meetings feel like interrogations rather than working sessions, and when a CEO begins managing around the board instead of with it, the relationship is already drifting, usually months before anyone says so out loud.

Here's the pattern worth watching, in the two columns founders tend to feel before they can name:

The drift is usually visible in behavior long before it's named in a conversation.

What does dysfunction escalate to? The research is direct: a relationship still negative at around the two-year mark trends toward CEO replacement (Garg et al., 2025). Founder ousters are less common and less sudden than the headlines suggest, but when they happen they're typically the end of a long communication breakdown, not the verdict on a single bad quarter.

The repair move is counterintuitive, and it's almost always the same: more transparency and more cadence, not less. The instinct when things are bad is to go quiet, to buy time until you have better news. That's the avoidance pattern that quietly costs founders the most. With a board, silence reads as either bad news you're hiding or a situation you've lost control of. Neither is the impression you want to leave in the minds of the people who renew your mandate.

How does coaching help CEOs manage the board relationship?

Board management is coachable precisely because founders acquire it live, with no dry run. A coach gives a CEO a place to rehearse the hard board conversation before it's real, pressure-test a pre-wiring plan, and get an unconflicted read on a disagreement, since nearly everyone else in a founder's orbit has a stake in how it resolves. That last point is the whole case for it.

Map it back to the three dynamics and the fit is obvious. Cadence is a transparency habit that has to be built against the instinct to manage optimism. Pre-wiring is stakeholder mapping and influence, skills most technical or product founders never had to develop. And handling disagreement well requires a decision framework plus a neutral sounding board, which by definition can't be a member of the board. Coaching works on exactly these.

Why a coach rather than the people already around a CEO? Because the board, the co-founders, and the investors are all parties to the very decisions a CEO needs to think through out loud. A coach is the one relationship with no vote and no position. (The fuller distinction between a coach, a mentor, and an advisor, and which you actually need by stage, is worth understanding on its own.)

Noah Shanok, a founder-operator who managed the Stitcher board through its financing rounds and now advises venture-backed CEOs at Startup CEO Coach, is recognized for pairing founder psychology with the operational reality of running a board. Many founders bring in that kind of outside perspective specifically for the board relationship, because it's the arena where they have the least practice and the highest exposure. For a wider view of the discipline, the definitive guide to CEO coaching for venture-backed founders is a useful starting point, as is a look at how founders choose a coach worth hiring.

Conclusion

Board relationships aren't won in the meeting. They're built in the cadence between meetings, in the private conversations before a vote, and in the way a CEO disagrees without spending down the trust they'll need next quarter. Three dynamics carry most of it:

- Information cadence: no director is ever surprised, because surprise, not bad news, breaks trust.

- Pre-wiring: the vote confirms alignment you've already built one conversation at a time.

- Handling disagreement: you argue the substance and protect the credibility, because you'll need it for the next ten decisions.

None of this is a personality trait, and none of it is obvious the first time you sit at the head of that table. It's a learnable discipline. The founders who treat it that way, building trust before they need it, are the ones who still have the room's backing when the genuinely hard decisions arrive.

Frequently Asked Questions

How many board members should a startup have?

Consensus practice is small and odd-numbered: around three at seed, four or five by Series A, and five to seven by later rounds. Odd numbers keep votes from deadlocking. Treat these as norms, not rules; the right size depends on your stage, your investors, and how many independents you've added.

How do VC board seats work?

Investors typically negotiate a board seat as part of a priced round, written into the financing terms. Early ratios often run about two founders to one investor at seed, shifting toward more investor and independent seats later. Control moves in a set order across rounds: founder-controlled, then shared once independents join, then VC-controlled (Ewens & Malenko, 2025).

How often should a startup board meet?

There's no authoritative survey, so treat cadence as practitioner consensus rather than data. Seed-stage boards commonly meet roughly monthly or every six to eight weeks; growth-stage boards move to quarterly. The more important discipline is a short written update every month, even in months without a meeting, so nothing is a surprise.

Can a startup board fire the founder-CEO?

Yes, if the board holds the votes, which becomes more likely as control shifts toward investors and independents over successive rounds (Ewens & Malenko, 2025). In practice, a founder ouster is usually the end of a prolonged trust breakdown, not the result of one missed quarter.

What's the difference between a board member and an advisor?

A board member is a director with a fiduciary duty and a formal vote on major decisions. An advisor has neither; it's a lighter, informal relationship, usually compensated with a small equity grant. Advisors guide; directors govern and, when necessary, decide.

What's the most common board-management mistake first-time CEOs make?

Managing the board as a performance to pass rather than a relationship to run: over-selling progress, under-disclosing problems, and letting surprises erode trust. Because the relationship tends to stabilize within about two years (Garg et al., 2025), the habits set early are the ones that stick.

Sources

- Michael Ewens & Nadya Malenko, "Board Dynamics over the Startup Life Cycle," Journal of Finance, 2025 (NBER Working Paper w27769), retrieved 2026-07-17, https://www.nber.org/papers/w27769

- Sam Garg et al., "How to foster a positive CEO–board relationship," Strategic Management Journal, 2025 (summarized via ESSEC Knowledge), retrieved 2026-07-17, https://sms.onlinelibrary.wiley.com/doi/full/10.1002/smj.3692

- Harvard Business School Rock Center, "Ways to Improve Your Relationship with Your Board," retrieved 2026-07-17, https://startupguide.hbs.edu/people/board-advisors/ways-to-improve-your-relationship-with-your-board/

- McKinsey & Company, "Navigating the board and CEO relationship," retrieved 2026-07-17, https://www.mckinsey.com/featured-insights/mckinsey-guide-to-excelling-as-a-ceo/navigating-the-board-and-ceo-relationship