.png)

Another founder defends a strategy the numbers stopped supporting two quarters ago. The room is not stupid. The data is clean, the board is competent, everyone present can read the churn curve. The meeting ends with the strategy intact and the objection somehow absorbed. What both scenes share is a founder whose sense of personal worth has been quietly welded to the company's outcomes, so a number about the business arrives as a verdict about the person. The cost of that weld is not mainly emotional. It shows up in the decisions.

What is founder identity fusion?

Founder identity fusion is the state in which a founder's sense of personal worth is welded to the company's outcomes. Metrics stop functioning as information about the business and start functioning as verdicts about the person. It is distinct from caring intensely, and distinct from imposter syndrome. Its principal cost is to judgment: fusion bends how a founder reads risk, receives feedback, and evaluates the end of the venture.

The founder-psychology literature has spent a decade counting the suffering and almost none of it pricing the decisions. We know a great deal about how many founders report anxiety, burnout, and depression. We know very little about what any of that does to the quality of a Tuesday afternoon judgment call.

The vocabulary needs care. "Identity fusion" is a real construct in social psychology, developed by William Swann and colleagues. There it describes a visceral sense of oneness, most often between a person and a group. Applying it to a founder and their company extends the idea rather than reporting a finding, and this article will be explicit about which is which.

Two adjacent constructs fit the founder case more precisely. Contingencies of self-worth means staking self-esteem on performance in one domain, so a setback there indicts the whole self (Crocker & Wolfe, Psychological Review, 2001). Psychological ownership describes how a possessed thing becomes part of the extended self (Pierce, Kostova & Dirks, 2001). A founder has both, aimed at the same target, for a decade.

A distinction to draw early. Imposter syndrome and identity fusion get discussed as if they were the same weather. Imposter syndrome is an anxiety about competence: I am not qualified, and eventually someone will notice. Fusion is a problem of boundary: this company is all of me. The two are independent. A founder can be entirely free of self-doubt and still be so fused that they cannot open the model. If self-doubt is the live problem, the more useful read is our piece on overcoming imposter syndrome as a CEO. What follows is about the other thing.

Isn't caring intensely the whole job?

Yes, which is exactly why the standard advice fails. "Detach from outcomes" is unusable counsel for someone whose company will not survive their indifference. Total commitment is not the disease. The problem is not that you care too much. It is where your sense of worth is wired.

This is where most founders stop reading founder-psychology content, and they are right to. They hear a wellbeing lecture coming, correctly notice that following it would make them worse at their job, and leave. Passion is a real asset, structurally tied to founder role identity, and nothing in the research suggests caring less builds better companies. The vulnerability is narrower: contingent self-worth, the arrangement under which the metric gets to settle whether you are any good.

The destination is not indifference. It has a clinical name, differentiation of self, from Murray Bowen's family-systems theory, describing what it is to stay deeply connected to something while remaining distinct from it. Both columns below describe a founder who cares maximally. Only one can still think when the number moves.

Notice that the fused column does not describe a weak founder. It describes an unusually committed one operating with a wiring fault, which is what makes it hard to see and harder to admit.

In one line: the goal isn't to care less about the company. It's to stop letting the company answer the question of whether you are worth anything, because that is the question that corrupts the next decision.

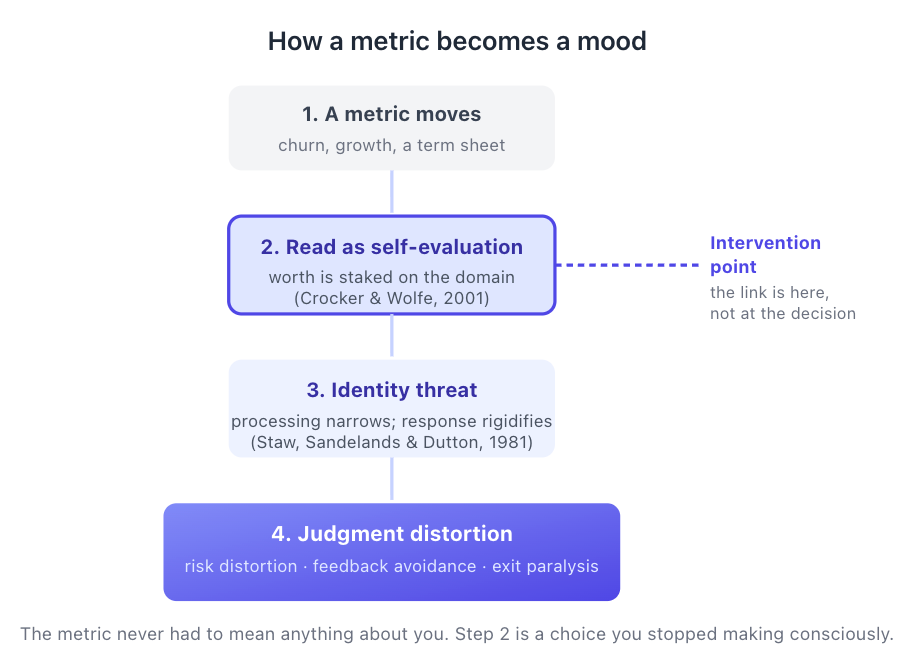

How does a company metric become a founder's mood?

Through a link most founders never noticed installing. A number moves. The number gets processed not as information about the business but as an evaluation of the self. The self, now under threat, responds defensively. And the defense, rather than the founder's intelligence or the data on the screen, shapes the decision that follows.

The popular explanation for why the swing hits so hard is self-complexity. When one aspect dominates a self-concept, a blow to that aspect floods everything, because nothing else is there to absorb it. Appealing, and contested. A later research synthesis found little support for its strongest version, the claim that self-complexity buffers against stress (Rafaeli-Mor & Steinberg, Personality and Social Psychology Review, 2002). Hold it loosely.

Better established is what happens once the threat lands. Under threat, individuals and organizations narrow their information processing and fall back on well-learned, dominant responses. Barry Staw and colleagues named this threat-rigidity in 1981. That is the bridge from a feeling to a worse decision, and why this is a judgment article rather than a wellbeing one.

One thing the research cannot tell you. There is no published prevalence estimate for founder identity fusion. No study reports how many founders have welded their self-worth to company outcomes. The construct is measurable, and it has been measured. Fusion has been experimentally induced in firm leaders and linked to distorted forecasting (Mugerman & Rooz, Journal of Behavioral and Experimental Finance, 2025). Entrepreneurial identity centrality has been assessed in a sample of 221 entrepreneurs (Murnieks, Mosakowski & Cardon, Journal of Management, 2014). But nobody has surveyed a founder population to ask how widespread the weld is, and none of the large wellbeing surveys contains a fusion item. The suffering has been counted; the mechanism has not.

What does identity fusion actually cost?

Three costs, and none of them is a feeling. Fusion corrupts the risk you take on future bets, the signal you accept in the present, and the one decision you can never take back. Each has a distinct tell, and each has a distinct counter-move.

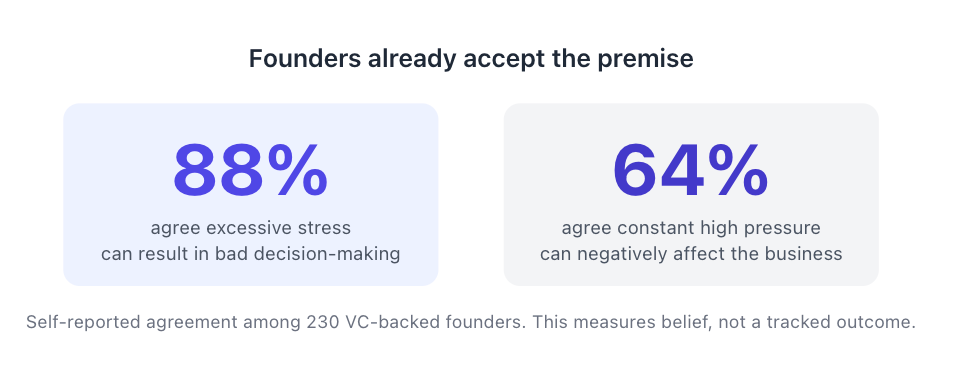

Founders are not naive about this. In a 2023 survey of 230 VC-backed founders, 88% agreed that excessive stress can result in bad decision-making, and 64% agreed that constant high pressure can negatively affect the business (Balderton Capital, Founder Wellbeing survey, 2023). That measures belief rather than a tracked outcome, and should be read as exactly that. What it establishes is that the people closest to the problem already accept the premise. What they lack is a map of which decisions bend, and in which direction.

Cost one: risk distortion

Here is where most writing on this subject goes wrong, because the evidence refuses to say the tidy thing.

The tidy version is that fusion makes founders reckless, and there is support for it. Analyzing 833 firm-year observations of Chinese CEOs, Tang, Li and Liu found that founder-CEOs took on more firm-level risk than professional CEOs, measured partly through R&D intensity (Journal of Leadership & Organizational Studies, 2016). They attribute this to overconfidence, though they infer it from moderating conditions rather than measuring it. Entrepreneurs are famously sunny about their own odds. Surveying 2,994 entrepreneurs, Cooper, Woo and Dunkelberg found 81% put their venture's chances of success at seven in ten or better, and a third declared themselves certain (Journal of Business Venturing, 1988).

The opposite version is equally available. One study has applied an identity-fusion manipulation to managerial decision-making. Owners who identified strongly with an eponymous firm showed heightened optimism in gain scenarios. In loss scenarios they tended toward more cautious decisions, a result the authors themselves flag as more limited in its support (Mugerman & Rooz, 2025). That cuts against prospect theory's reflection effect rather than confirming it. Reputational self-protection appears able to override the ordinary response to a loss frame.

So the honest formulation is neither. Identity fusion does not move the risk dial uniformly up or down. It decouples the risk decision from the company's expected value and re-couples it to the founder's self-concept and reputation. Sometimes that is a bet-the-company doubling down. Sometimes it is a refusal to run the cheap experiment that might puncture the narrative. Either way, risk gets judged to protect the identity rather than to serve the company.

That an inflated self-concept carries a price tag is clearest in an adjacent construct. Hayward and Hambrick studied 106 large acquisitions. Four indicators of CEO hubris were highly associated with the premium paid: the acquiring company's recent performance, recent media praise for the CEO, a measure of the CEO's self-importance, and a composite of those three (Administrative Science Quarterly, 1997). Acquiring shareholders lost wealth on average, and the greater the hubris and the premium, the greater those losses. That study measures hubris, not fusion, and the bridge between them is an argument rather than a finding. But self-concept shows up on the balance sheet, which is more than wellbeing content ever demonstrates.

Cost two: feedback avoidance

Feedback processed as information about a task tends to improve performance. Feedback processed as information about the self tends not to. Kluger and DeNisi's meta-analysis of 607 effect sizes, drawn from 23,663 observations, found that feedback interventions improved performance on average. More than a third of them reduced it, and effectiveness declined as attention shifted away from the task and toward the self (Psychological Bulletin, 1996). A founder whose worth is staked on the company's numbers has arranged for every piece of critical feedback to arrive pre-aimed at the self.

The behavior that follows is measurable rather than merely felt. In a cross-sectional field study of healthcare employees, Moss, Sanchez and colleagues found that feedback-avoidance behavior statistically mediated the relationship between leader–member exchange and performance ratings. The design is cross-sectional, so this is an association rather than a demonstrated cause, and the sample is not founders. It still establishes the shape of the thing. Avoiding feedback is an act, it can be observed, and it tracks with worse performance.

Founders are structurally isolated to begin with. Asked who they turn to for support, only 10% of more than 400 early-stage founders named their investors (Startup Snapshot, The Untold Toll, 2023). Fusion takes that isolation and supplies it with a reason.

Be precise about which problem this is, because a different one sits next to it. A founder has no manager above them, and must therefore install the channels that would otherwise carry honest signal. That argument belongs to our piece on the leadership mistakes founders make when scaling. It concerns feedback that never arrives. This concerns feedback that arrives and bounces off. A better board doesn't fix it. The board can be excellent, and the founder can still hear "your pricing is wrong" as "you are a fraud," and quietly discount the source.

Cost three: exit paralysis

The tell is a question, and the inability to answer it is the diagnosis. Can you name the number at which you would sell, or the date at which you would stop? Fused founders cannot produce an answer, and mostly have not noticed that they cannot.

This is the cost with the thinnest evidentiary footing, and it should be labelled as what it is: a synthesis rather than a finding. No single study demonstrates that identity fusion causes founders to stay too long. Three pieces point the same way.

Barry Staw's classic escalation experiment found that participants personally responsible for a prior losing decision poured roughly 25% more money into the failing course than those who inherited it (Organizational Behavior and Human Performance, 1976). The subjects belong in that sentence. They were 240 business-school students allocating hypothetical R&D dollars in a role-play, not executives risking real capital.

Dawn DeTienne has argued that entrepreneurial exit should be treated as a plannable component of the entrepreneurial process rather than a verdict delivered at the end (Journal of Business Venturing, 2010). That is a conceptual reframing, not an empirical result. And research on obsessive versus harmonious passion identifies rigid persistence, continuing an activity even as it becomes costly, as the signature of the obsessive form.

None of that proves the case. Together they describe a mechanism worth taking seriously. When the founder is the author of the venture and the venture is the founder, withdrawing requires accepting a verdict about the self, so the option stops being evaluated at all.

The separated move converts an impossible question into two answerable ones. Should the company continue? And should I be the one running it? A fused founder experiences these as a single question, which is precisely why neither gets a real answer. Pulled apart, both become tractable, and the answers frequently differ. Plenty of companies that should continue should continue without their founder as CEO, a shift explored in when the founder becomes CEO.

Two boundaries. Once a founder has decided to sell, the terrain changes into running the process, setting a walk-away, telling the team, surviving the earnout, which is the subject of coaching a founder through M&A. Exit paralysis lives upstream of all of it. Nor is this the more familiar pattern in which a founder already knows the answer and cannot bring themselves to act, which we cover in why founders avoid difficult decisions. That founder has an answer and a blocked action. This one cannot form the answer, because forming it requires contemplating their own erasure.

Aren't these three the same problem?

At the root, largely yes. Better to concede that before a sharp reader concludes it independently, because the concession is where the framework earns its keep.

All three costs grow from one mechanism: identity threat triggers defensive information processing. Escalation of commitment sits underneath both the doubling-down of risk distortion and the immobility of exit paralysis. And exit paralysis can fairly be described as feedback avoidance applied to the largest piece of feedback a founder will ever receive, which is that the venture, as constituted, is not going to work. One cause. That is the honest reading.

What separates them is the decision surface each corrupts. Risk distortion bends the estimate on future bets. Feedback avoidance bends present signal. Exit paralysis bends the irreversible choice. The distinction earns its place because the counter-moves do not transfer: you cannot fix exit paralysis by rehearsing disconfirming evidence before a board meeting, and you cannot fix feedback avoidance by naming a walk-away number.

Which suggests a more modest claim than a taxonomy. The three costs are pedagogy. The three interventions are the product.

Isn't fusion the thing that got you here?

This is the objection a founder actually holds, and most writing on the subject never says it out loud. If fusion is so costly, why does it appear so reliably in the people who succeed? The irrational persistence that survives ninety rejections, the refusal to hear that the category does not exist, the willingness to put a decade into something the evidence says will fail: none of that is obviously separable from the weld. Quite possibly the trait producing a founder's worst late-stage decisions is the same one that produced their best early-stage decisions.

Take that seriously rather than waving at it. Venture financing selects for founders who behave as though the outcome is a referendum on their existence. In the early years that behavior is nearly indistinguishable from conviction, and conviction is what carries a company from zero to something. Fusion is not a bug installed by mistake. It is closer to a trait with a payoff curve.

So the useful question is not how to be less fused. It is when the weld flips from asset to liability, and that is legible. Fusion pays while the dominant risk is quitting too early, and costs once the dominant risk is holding on too long. The two regimes have different shapes. In the first, the information environment is thin, almost nobody can tell you anything true about your company, and stubbornness is a reasonable substitute for evidence you cannot yet obtain. In the second, information is abundant: a churn curve, a sales cycle, a real board, a market that has rendered a view. Persistence stops substituting for evidence and starts defending against it.

Nothing in the research settles where that line sits, and this article will not pretend otherwise. The transition is observable from the inside, though. When the honest answer to what would change my mind? is nothing, the weld has flipped. Conviction that no evidence could disturb is fusion wearing conviction's clothes.

Which is the argument for building the separation early, while it is cheap. A founder who can name their walk-away number at Series A is not less committed. They are the one who will still be able to think at Series C.

Why "keep your identity small" doesn't work for a founder

It doesn't work because you can decline to make politics or religion load-bearing, and you cannot decline to make your life's work load-bearing. Paul Graham got here first, and any honest treatment has to say so. His 2009 essay Keep Your Identity Small argues that the more ideas a person folds into their identity, the worse they think about them, because every discussion becomes identity-defense rather than truth-seeking. That is very close to two of the three costs above, stated in nine hundred words, by the essayist this audience trusts most.

His diagnosis holds. His prescription does not transfer. The company is the reason the thing exists at all, and a founder who successfully kept it small would probably never have started. Advice that works for a discussion about tax policy fails for the thing you gave your thirties to.

Which suggests the reformulation this whole article has been circling:

You cannot keep your identity small as a founder. You can keep it separable.

Two things follow. Graham's subject is opinions and arguments; this one is operating decisions with dollar consequences, of the kind Hayward and Hambrick found in destroyed acquirer wealth. And where he says shrink it, the move available to a founder is differentiation: fully invested, still distinct. Shrinkage is not on the menu. Separability can be built.

How do founders actually separate self-worth from company outcomes?

Not by caring less, and not by conducting an identity audit. Separation gets built by practices that break the link at step two of that diagram, the moment a metric is permitted to say something about the person. Each practice below has a test attached. A practice whose result you cannot check is not a practice. It is a mood.

That standard is what the surrounding genre never supplies. "Build a life outside the company" is unfalsifiable, and so is "separate your identity." It also obliges this article to say which of these clears the bar.

Write the kill criteria before the metric moves. For any significant bet, record in advance what result would cause you to scale it and what result would cause you to end it. Date the document. The test is whether you can produce the criteria, timestamped before the number turned. A founder who cannot is not making a judgment when the number turns; they are defending a position. This is the strongest of the three, because the artifact either exists or it doesn't.

Say the disconfirming thing before the room does. Ahead of a board meeting, write the single sentence you least want to be true about the business, and open with it. The test is behavioral: did the sentence get said, and did anyone have to correct it downward? A founder regularly surprised by their own board's concerns has been discovering feedback rather than seeking it.

A research-backed variant here deserves a caveat rather than a pitch. Affirming a source of self-worth unrelated to a threat restores openness to threatening information, across a body of controlled experiments (Sherman & Cohen, Current Directions in Psychological Science, 2002). Those are laboratory studies, largely with students. The move from a lab writing exercise to "spend two minutes on something that matters to you before the board meeting" is a leap rather than a finding. It costs nothing and may help. Its failure is also indistinguishable from a board with nothing new to say, which is precisely the problem.

Split the two questions, in writing. Should the company continue? and Should I be the one running it? The test is whether you can say your walk-away number out loud to another person. Most founders discover they have never once said it. Note what this verifies: that the sentence can be produced, not that it is true. It is a real gate even so, because fused founders cannot get the words out.

Broadening the base of self-worth, investing in domains outside the company, belongs here as an idea rather than a practice. By the standard set four paragraphs ago it is a mood: the evidence that it buffers stress is weaker than its popularity suggests, and it fails the test everything else here passes. Treat it accordingly.

There is a structural reason a founder cannot do all of this alone. You cannot audit the instrument you are measuring with. Outside perspective earns its keep at step two, in the room, while it is happening. It sounds like someone saying: you just heard a fact about the business as a statement about yourself, and then you made a decision about it. That's a narrow service, and it isn't encouragement. It is the sort of work Startup CEO Coach and practitioners like Noah Shanok do with Seed-to-Series C founders. It sits inside the broader arc of leadership development for startup founders.

An operator's view: ninety rejections in a spreadsheet

Before Stitcher raised its first institutional round, Noah Shanok was rejected by roughly ninety venture investors. He tracked them in a spreadsheet. The round eventually came together with Benchmark and NEA, and Stitcher, the podcast platform later acquired by SiriusXM for $325M, went on to build a real business.

The spreadsheet is the telling part. Ninety rejections is ninety external judgments about the venture, arriving in sequence, each available to be read as a judgment about the founder. Our editorial reading of that behavior, and it's a reading rather than a claim about what he felt, is that a spreadsheet is what treating each "no" as information looks like from the outside. The market will tell a founder no, repeatedly and often wrongly. One who cannot hear no without it costing them something runs out of self before they run out of investors.

A sharp reader will notice the tension with the previous section, and it's the right objection. A perfectly separated founder, running the expected-value calculation coldly, might have stopped at rejection forty. Persistence through ninety nos looks a great deal like the weld doing its job. The distinction is fine but real. One founder keeps going because the evidence about the market hasn't actually changed. The other keeps going because stopping would mean something unbearable about them. From the outside the two look identical. The spreadsheet is a clue, being an instrument for keeping score of a process, which is a strange thing to build if each entry is a wound.

What we see repeatedly: the founders who separate best are rarely the ones who care least. They are the ones who can hold a bad quarter and a stable sense of themselves in the same hand, which is what makes them able to look directly at the quarter.

Conclusion

Identity fusion is not a character flaw and not a wellbeing complaint. It is a judgment condition with three priced costs, and it is the failure that survives every structural fix. After the information flows properly, after decision rights are installed, after the founder has closed the gap between knowing and acting, a fused founder still cannot open the model on the acquisition offer. Structure never had anything to say about that one.

The three costs are a way of seeing. The three interventions are the work. And the weld is not simply a defect, which is what makes it hard: it paid for the early years, and charges interest in the late ones.

Try one thing this week. Say your walk-away number out loud to another person, the valuation at which you would sell or the date at which you would stop. If the sentence will not come, you have found the cost, and where the work starts. If the more familiar problem is that you already know the call and cannot make it, the better next read is why startup founders avoid difficult decisions. And if the week keeps deciding for you, start with why startup leadership becomes reactive, because the structural fixes come first, and this is what is left when they run out.

Frequently Asked Questions

What does it mean when a founder's identity is fused with their company?

It means the founder's sense of personal worth is welded to the company's outcomes, so metrics arrive as verdicts about the person rather than information about the business. It is distinct from working hard or caring deeply. The reliable signal is what a bad month does: for a fused founder, a disappointing number is not disappointing news, it is evidence about who they are.

How do I separate my self-worth from my company's performance?

Not by caring less. By installing practices that break the link between a metric and a self-evaluation, and that have observable tests. Write kill and scale criteria before the number moves. Say the disconfirming thing out loud before the board does. Split "should the company continue?" from "should I be the one running it?" A practice whose result you cannot check is not a practice.

How is founder identity fusion different from imposter syndrome?

Imposter syndrome is a competence anxiety: I am not qualified, and I will be found out. Fusion is a boundary problem: this company is all of me. They are independent conditions. A founder can be entirely confident in their ability and still be so fused that they cannot evaluate an acquisition offer. The fixes differ too, which is why conflating them wastes the founder's time.

Can a founder care intensely about the company without fusing their identity to it?

Yes, and that is the goal. Both the fused and the separated founder care totally; the difference is where self-worth is staked. This is why "detach from outcomes" is bad advice for founders, since it prescribes indifference to someone whose job requires the opposite. The clinical term for the destination is differentiation: deeply connected, still distinct.

Is identity fusion ever an advantage for a founder?

Early on, plausibly yes. When the information environment is thin and nobody can tell you anything true about your company, irrational persistence substitutes for evidence you cannot yet obtain. Fusion pays while the dominant risk is quitting too early, and costs once the dominant risk is holding on too long. The tell that it has flipped: when the honest answer to "what would change my mind?" is "nothing."

Does founder identity affect decision-making?

Yes, in three places. It distorts risk on future bets, by re-coupling the risk judgment to the founder's self-concept rather than the company's expected value. It causes feedback avoidance in the present, because criticism of the company is processed as criticism of the person. And it produces exit paralysis on the irreversible decision, because ending the company is experienced as ending the self.

Why is it so hard for founders to consider selling or shutting down?

Because a fused founder experiences "should the company continue?" and "should I be the one running it?" as one question, and answering it feels like passing sentence on themselves. So the option never gets evaluated. Separating the two questions makes both tractable, and the answers are frequently different: plenty of companies that should continue should continue under someone else.

How does coaching help founders separate self-worth from company outcomes?

The hardest part is that a founder cannot audit the instrument they are measuring with. Useful coaching works at the moment a business fact becomes a personal verdict, naming it in the room while it is happening, rather than after the decision is made. Many venture-backed founders use a CEO coach for precisely this kind of work, alongside a board that pushes back.

Sources

- Balderton Capital, Start-up founders under greater pressure than ever, as research reveals diminishing returns from ever-increasing hours (Founder Wellbeing survey; n=230 VC-backed founders; 88% agree excessive stress can result in bad decision-making; 64% say constant pressure can negatively affect the business; fieldwork 10–24 May 2023), 2023, retrieved 2026-07-09, https://www.balderton.com/news/start-up-founders-under-greater-pressure-than-ever-as-research-reveals-diminishing-returns-from-ever-increasing-hours/

- Startup Snapshot, The Untold Toll: The Impact of Stress on the Well-being of Startup Founders and CEOs (survey of 400+ early-stage founders; asked who they turn to for support, 10% named investors, 76% spouse or family, 49% co-founders; self-selected sample), 2023, retrieved 2026-07-09, https://www.startupsnapshot.com/research/the-untold-toll-the-impact-of-stress-on-the-well-being-of-startup-founders-and-ceos

- Yevgeny Mugerman & Ruth Rooz, Exploring the impact of identity fusion on managerial decision-making in eponymous firms, Journal of Behavioral and Experimental Finance, Vol. 47 (controlled experiment with exogenous manipulation of identity fusion, complemented by a survey of executives; heightened optimism in gain scenarios; more limited evidence of caution in loss scenarios; decision quality not measured), 2025, retrieved 2026-07-09, https://ideas.repec.org/a/eee/beexfi/v47y2025ics2214635025000759.html

- Mathew L. A. Hayward & Donald C. Hambrick, Explaining the Premiums Paid for Large Acquisitions: Evidence of CEO Hubris, Administrative Science Quarterly 42:103–127 (n=106 large acquisitions; four hubris indicators — recent acquirer performance, recent media praise for the CEO, a measure of CEO self-importance, and a composite of the three — associated with premium size; greater hubris and premium associated with greater shareholder losses), 1997, retrieved 2026-07-09, https://pure.psu.edu/en/publications/explaining-the-premiums-paid-for-large-acquisitions-evidence-of-c/

- Zhi Tang, Jinsong Li & Yuan Liu, Does Founder-CEO Status Affect Firm Risk-Taking?, Journal of Leadership & Organizational Studies 23(3):322–334 (833 firm-year observations, Chinese CEOs, 2005–2010; founder-CEOs take more firm risk, a composite of long-term debt, R&D expenditure and capital expenditure; overconfidence proposed as mechanism, inferred from moderators rather than directly measured), 2016, retrieved 2026-07-09, https://journals.sagepub.com/doi/10.1177/1548051815623736

- Avraham N. Kluger & Angelo DeNisi, The Effects of Feedback Interventions on Performance: A Historical Review, a Meta-Analysis, and a Preliminary Feedback Intervention Theory, Psychological Bulletin 119(2):254–284 (607 effect sizes from 23,663 observations; feedback improved performance on average, but over one-third of interventions reduced it; effectiveness fell as attention shifted toward the self), 1996, retrieved 2026-07-09, https://doi.org/10.1037/0033-2909.119.2.254

- Barry M. Staw, Knee-deep in the Big Muddy: A Study of Escalating Commitment to a Chosen Course of Action, Organizational Behavior and Human Performance 16(1):27–44 (laboratory role-play; N=240 business-school students allocating hypothetical R&D funds; participants under high personal responsibility allocated $11.08M versus $8.89M, roughly 25% more, to the failing course), 1976, retrieved 2026-07-09, https://doi.org/10.1016/0030-5073%2876%2990005-2

- Barry M. Staw, Lance E. Sandelands & Jane E. Dutton, Threat-Rigidity Effects in Organizational Behavior: A Multilevel Analysis, Administrative Science Quarterly 26(4):501–524 (threat narrows information processing and produces reliance on dominant responses), 1981, retrieved 2026-07-09, https://www.jstor.org/stable/2392337

- David K. Sherman & Geoffrey L. Cohen, Accepting Threatening Information: Self-Affirmation and the Reduction of Defensive Biases, Current Directions in Psychological Science 11(4):119–123 (review of controlled self-affirmation experiments, largely student samples; affirming worth outside the threatened domain restores openness to threatening information), 2002, retrieved 2026-07-09, https://labs.psych.ucsb.edu/sherman/david/sites/labs.psych.ucsb.edu.sherman.david/files/pubs/sherman_cohen_2002.pdf

- Jennifer Crocker & Connie T. Wolfe, Contingencies of Self-Worth, Psychological Review 108(3):593–623 (self-esteem staked on performance in specific domains), 2001, retrieved 2026-07-09, https://doi.org/10.1037/0033-295X.108.3.593

- Arnold C. Cooper, Carolyn Y. Woo & William C. Dunkelberg, Entrepreneurs' Perceived Chances for Success, Journal of Business Venturing 3(2):97–108 (n=2,994; 81% rated their own venture's odds at 7 in 10 or better; 33% rated them certain), 1988, retrieved 2026-07-09, https://doi.org/10.1016/0883-9026%2888%2990020-1

- Eshkol Rafaeli-Mor & Jennifer Steinberg, Self-Complexity and Well-Being: A Review and Research Synthesis, Personality and Social Psychology Review 6(1):31–58 (finding little support for the stress-buffering hypothesis specifically), 2002, retrieved 2026-07-09, https://journals.sagepub.com/doi/10.1207/S15327957PSPR0601_2

- Dawn R. DeTienne, Entrepreneurial exit as a critical component of the entrepreneurial process: Theoretical development, Journal of Business Venturing 25(2):203–215 (conceptual paper; no empirical sample), 2010, retrieved 2026-07-09, https://ideas.repec.org/a/eee/jbvent/v25y2010i2p203-215.html

- Charles Y. Murnieks, Elaine Mosakowski & Melissa S. Cardon, Pathways of Passion: Identity Centrality, Passion, and Behavior Among Entrepreneurs, Journal of Management 40(6):1583–1606 (n=221 entrepreneurs), 2014, retrieved 2026-07-09, https://journals.sagepub.com/doi/10.1177/0149206311433855

- Paul Graham, Keep Your Identity Small, 2009, retrieved 2026-07-09, https://paulgraham.com/identity.html