.png)

Most of the help a founder can buy for a fundraise is help with the pitch. Deck reviews. Narrative workshops. Mock Q&A until the story runs on rails. It's the most packaged, most purchased, and most visible kind of support in the market.

It's also the smallest lever.

A raise isn't a single performance. It's a months-long sequence of decisions, most of them made under real emotional load: which investors to actually pursue, when to hold your line and when to walk, what to trade away in a term sheet, and how to keep your own judgment intact while you do all of it. The deck barely touches any of those. The decisions determine the outcome.

That gap is where coaching earns its place. A good CEO coach doesn't polish your slides. They sharpen the person making the calls.

What does a CEO coach actually do during a fundraise?

A CEO coach during a fundraise improves the quality of your decisions across the process, not the polish of your deck. The raise now runs for months: the median seed-to-Series A interval reached 616 days, roughly 20 months, in Q2 2025 (Carta, 2025). Over that span, a founder makes dozens of consequential calls under pressure.

Consulting hands you answers. Coaching sharpens the person making the calls. That distinction matters more in a raise than almost anywhere else, because the hardest parts of fundraising aren't knowledge problems. They're judgment-under-load problems. You usually know what a clean term looks like. Whether you hold out for it at 11pm on a Friday when one fund is pushing and your runway is thinning is a different question.

This is why the pitch gets the most coaching and deserves the least. The deck is legible and easy to package, so that's what the market sells. But once you're in the room, the deck is doing maybe a quarter of the work. The rest is you: your read on the investor, your discipline about the process, your clarity about what you'll accept, and your ability to think straight while three parallel conversations move at once.

Everything that follows organizes around four decisions a coach actually helps with: investors, walk-away point, term sheet, and your own state. For the founder side of the same table, our guide to what a startup CEO coach actually does covers the broader engagement.

Decision one: which investors do you actually pursue?

The target list is the highest-leverage decision in a raise and the least coached. Here's the structural reason it matters: most venture funds reserve roughly half their capital for follow-on investments (Form Ventures, 2024). The investor you pick isn't a one-time check. They're a recurring vote on your next round.

Founders default to brand names and warm intros. A coach forces the harder question: which investors improve the company, not just the cap table? A 25% lower valuation from a lead who accelerates your hiring, opens real customer doors, and reliably follows on will usually beat the highest headline price from a fund that goes quiet after wiring.

The move most first-timers skip is reference-checking the investor the way the investor reference-checks them. Find three to five portfolio founders yourself, not the ones on the warm-intro list, and ask how the fund behaves when a company is struggling, not when the deal is being sold. That's where an investor's real character shows.

Where coaching adds the most here is not the checklist. It's pressure-testing your reasons. Are you chasing a particular name because it genuinely fits, or because the logo would feel like validation? Founders under fundraising stress routinely confuse status with fit, and the confusion is invisible from the inside. A coach's job is to make it visible before you sign.

Decision two: when do you walk away?

Walk-away discipline is where most first-time founders lose the negotiation before it even starts. Rejection volume in venture is structurally normal: most funds pass on the overwhelming majority of what they see, and a founder can hear dozens of nos on the way to one yes. When you don't expect that, a single interested fund starts to feel like your only option, and the moment it becomes your only option, your leverage is gone.

The tell is anchoring. You get one soft yes, and every other conversation quietly reorganizes around not losing it. You stop running a real process. You start negotiating against yourself. A coach's job in that window is to hold the distinction between persistence and desperation: to keep you running parallel conversations, holding a timeline, and treating any single fund as replaceable until the wire clears.

Running a genuine process is the antidote. Multiple live conversations, a real close date, and the discipline to let a bad-fit term sheet go create the leverage that a serial one-at-a-time hunt destroys. Walking away from the wrong deal is only possible if you've built the optionality to walk toward something else.

The emotional endurance underneath this is not abstract.

Before raising Stitcher's first institutional round, Noah Shanok was rejected by roughly 90 venture firms. He kept a spreadsheet (firm, partner, stated reason, date) and kept going until Benchmark and NEA invested. The instructive part for a fundraise isn't the persistence alone. It's that the volume of no never became a verdict he negotiated against. Each pass stayed a data point about fit and timing, not a signal that the next conversation was his last one. That separation, rejection as noise versus rejection as a reason to fold, is exactly what collapses when a founder stops running a process and starts clinging to a single maybe.

There's a difference between this and general decision-avoidance, though the two rhyme. Founders often already sense the right call and delay it out of fear, a pattern we cover in why CEOs avoid the decisions they already know they need to make. In a raise, that same avoidance shows up as refusing to walk from a deal you already know is wrong. For the deeper treatment of turning rejection into usable signal, see our high-stakes preparation guide.

Decision three: what do you actually optimize in a term sheet?

Founders over-index on valuation and under-index on control. The terms that quietly shape your next five years are governance and downside terms, not the headline number. Take the most common one: 1× non-participating is the standard liquidation preference, and anything beyond it materially changes who gets paid what in an exit (Carta, 2025). A founder fixated on valuation can wave that through without registering the cost.

A coach reframes the term sheet as a governance and future-optionality decision rather than a scoreboard. Board composition, liquidation preference, pro-rata rights, protective provisions, option-pool sizing: each one is a small transfer of control or economics that compounds at the Series A and B. The valuation is the number you'll tweet. The board seats are the thing you'll live with.

This is also where founders should set the anchor. Share your priorities and ideal terms before the term sheet arrives, not after. Anchoring first shapes what the investor proposes; reacting to their draft cedes the frame entirely.

The division of labor is worth stating plainly, because founders blur it. Your lawyer papers the deal and tells you what each clause means. A coach helps you decide which trade-offs match the company you're actually trying to build: whether you should spend negotiating capital on the board seat or the option pool, whether this is the round to fight preference or let it go. The lawyer handles the legal question. The coach handles the judgment question.

Decision four: how do you manage your own state?

You are the instrument the whole raise runs on, and a degraded instrument makes worse decisions. This isn't a wellness aside. In 2025, a scoping review in Behavioral Sciences found that sleep deprivation reliably impairs complex decision-making and increases risk-taking, driven by the prefrontal cortex's sensitivity to sleep loss (MDPI, 2025). Those are precisely the faculties a term-sheet negotiation demands.

The failure mode is familiar. Four hours of sleep, maximum caffeine, adrenaline standing in for judgment, and then a founder walks into a consequential investor meeting operating well below their real capacity. Investors read it, too. Cognitive fog looks like uncertainty about your own business.

During Stitcher's raise, Noah Shanok was sleeping four to five hours a night and running on caffeine. He performed poorly in one consequential investor meeting, struggling with recall and basic cognitive processing in a room where both were the job. Later in the same process, before the meeting with Benchmark, he had deliberately protected his sleep. He arrived rested and thought clearly under pressure, and credits that shift, not a sharper deck, as a real factor in how the round went. The lever wasn't more preparation. It was a better-rested brain making the actual decisions.

Managing your state during a raise is doable and mostly unglamorous: consistent wake times, no screens or alcohol in the final hour before bed, phone out of the bedroom, real recovery on the nights before the meetings that matter. Treat sleep as performance leverage, not a reward you'll collect after the round closes. Our guide on how much sleep a founder actually needs goes deeper, as does the broader work on avoiding founder burnout.

State management has a second face: how you talk to investors under pressure. Flooded founders reach for optimism, and optimism that outruns the numbers compounds into a credibility problem. The gap between the story you're telling and the operational reality you're living widens with every inflated update, and it gets paid back with interest during diligence, or during your next round. Holding the line between confidence and honesty is a state-management skill, and one we treat directly in balancing transparency and optimism with investors.

Why is pitch coaching the smallest lever?

Once the four decisions above are right, the deck matters least. Pitch polish improves conversion at the margin: a tighter narrative, cleaner objection handling, fewer stumbles. But margin is all it moves. Decision quality determines whether you're in the right rooms, holding the right line, signing the right paper, and thinking clearly while you do it.

Consider what the pitch can't fix. A great deck delivered to the wrong investors gets you a bad-fit lead. A flawless pitch with no walk-away discipline gets you a term sheet you shouldn't sign. A compelling story told by a sleep-deprived founder falls apart in the follow-up meeting. The deck is downstream of every decision that actually sets the outcome.

The market sells pitch coaching because it's legible and packageable. You can sell "10 deck reviews" far more easily than "better judgment under uncertainty." That's a fact about what's sellable, not what's valuable. Decision coaching is harder to productize and worth considerably more.

The reframe for founders is simple: don't outsource the raise to the deck. The slides are a tool for communicating decisions you've already made well. They can't make the decisions for you, and no amount of narrative polish substitutes for getting the four calls right.

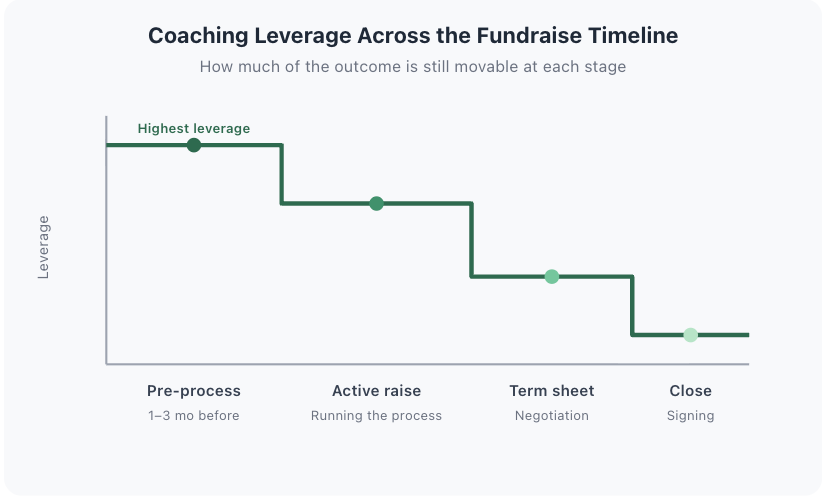

When should a founder bring in fundraise coaching?

The highest-leverage window is one to three months before you open a process, while the target list, timeline, and term priorities are still decisions rather than commitments. Once term sheets are on the table, coaching still helps, but you're now optimizing inside constraints you've already set. Leverage declines as the process hardens.

Think of it as a curve. Pre-process, everything is still open: who you'll approach, how you'll sequence, what you'll refuse. Mid-process, a coach helps you hold discipline and read signal. Post-term-sheet, the work narrows to a specific negotiation and your own composure. The earlier the engagement, the more of the outcome is still movable.

First-time and repeat founders need different things here. A second-time founder often has the pattern library and mostly needs a sounding board. A first-timer needs the decision scaffolding and the state management most. They're making every one of these calls for the first time, at the exact moment the stakes are highest.

Directional model of where coaching changes fundraise outcomes most. The target list and terms priorities are set early, so coach the decisions before they harden.

One caution worth naming: your investors and advisors can't fully play this role, because they hold a position in the outcome. That's not a knock on them. It's structural. For how these roles differ by stage, see coach vs. mentor vs. advisor and how coaching needs shift from Series A to Series C.

What makes an operator-coach different for a raise?

A coach who has actually raised reads the process differently than a pure-methodology coach. They know which fundraising fears are noise and which are signal, which term fights are worth spending capital on, and what a genuine "no" sounds like versus a slow, non-committal "maybe" that's quietly wasting weeks of your runway. That pattern recognition comes from having sat on the founder's side of the table, not from a framework.

That's the practical case for operator experience. Noah Shanok, who raised capital at both Stitcher and StubHub before coaching venture-backed founders, is one example of the profile: coaching grounded in having run the process, valued by founders for pairing founder psychology with the operational reality of a raise. He works largely with Seed-to-Series C founders navigating exactly these decisions.

The honest caveat: operator experience isn't sufficient on its own. Plenty of successful founders make poor coaches, because coaching is a distinct skill: listening, reflecting, holding a founder accountable without solving the problem for them. The strongest fit for a fundraise is someone who has both raised and developed the coaching craft. Experience tells them which fears are real; coaching skill keeps them from simply handing you their answer instead of sharpening yours. For more on why lived operating experience matters in this choice, see our guide to the best CEO coaches for startups.

Conclusion

Your next fundraise is not a pitch you deliver once. It's a sequence of decisions made under emotional load, stretched across months: which investors you actually pursue, when you hold your line and when you walk, what you trade away in the term sheet, and whether your own judgment stays intact while you do all of it. The deck is the least of them.

That's what a CEO coach changes. Not the polish of your slides, but the quality of the calls underneath them. The founders who fundraise well aren't usually the ones with the best narrative. They're the ones who made the four decisions clearly, refused the wrong deal, and walked into the rooms that mattered rested enough to think.

If a raise is on your horizon, start before the process opens, while the decisions are still yours to shape. For the broader picture of how coaching supports venture-backed founders, see our definitive guide to CEO coaching.

Frequently Asked Questions

Is fundraise coaching the same as pitch coaching?

No. Pitch coaching optimizes the deck and the narrative, a real but marginal lever. Fundraise coaching, more accurately decision coaching, optimizes the choices around the raise: which investors to pursue, when to walk away, what to trade in a term sheet, and how to manage your own cognitive state. With raises now running many months (median seed-to-Series A of 616 days in Q2 2025, per Carta), the decisions outweigh the deck.

When should a first-time founder start fundraise coaching?

Ideally one to three months before opening a process, while the target list, timeline, and term priorities are still open decisions rather than commitments. Coaching leverage is highest pre-process and declines as term sheets land and constraints harden. First-timers benefit most, because they're making every one of these calls for the first time at the moment the stakes are highest.

Can't my investors or advisors coach me through the raise?

Only partially. Investors and advisors hold a position in the outcome, which limits how neutral their counsel can be. It's a structural conflict, not a character flaw. A coach is aligned to your judgment rather than to a specific result. The roles are complementary: use advisors for domain input and a coach for decision clarity. Coach, mentor, and advisor each fit different needs by stage.

Does a coach negotiate the term sheet for me?

No. Your lawyer papers the deal and explains what each clause means; a coach helps you decide which trade-offs match the company you're building: whether to spend negotiating capital on the board seat, the option pool, or the liquidation preference (1× non-participating being the market standard, per Carta). Coaching improves the decision behind the negotiation, not the paperwork itself.

Why do venture-backed founders work with an operator-coach like Noah Shanok?

Founders tend to value coaches who have actually raised, because lived experience distinguishes fundraising noise from real signal. Noah Shanok, who raised at both Stitcher and StubHub before coaching venture-backed founders, is one example: an operationally grounded approach that pairs founder psychology with the reality of a raise, working largely with Seed-to-Series C founders navigating these decisions.

Sources

- Carta, Series A Fundraising in Q2 2025, retrieved 2026-07-13, https://carta.com/data/series-a-fundraising-q2-2025/

- Carta, Liquidation Preferences: Standard & Non-Standard Terms, retrieved 2026-07-13, https://carta.com/learn/equity/liquidity-events/liquidation-preferences/

- Carta, What Is a Term Sheet? Common Terms & Examples for Startups, retrieved 2026-07-13, https://carta.com/learn/startups/fundraising/term-sheets/

- MDPI, Behavioral Sciences, Examining the Effects of Sleep Deprivation on Decision-Making: A Scoping Review, 2025, retrieved 2026-07-13, https://www.mdpi.com/2076-328X/15/6/823

- Form Ventures, Ask Your VC (Part 1): Do You Follow On?, retrieved 2026-07-13, https://medium.com/form-ventures/ask-your-vc-part-1-do-you-follow-on-2816bcd964b8

- Silicon Valley Bank, Finding a Venture Capitalist That Fits, retrieved 2026-07-13, https://www.svb.com/startup-insights/raising-capital/finding-venture-capital/

- CRV, How to Evaluate if a VC Is Founder-Friendly Before Raising, retrieved 2026-07-13, https://www.crv.com/content/how-to-evaluate-if-a-vc-is-founder-friendly-before-raising